Invest

Investing involves challenges, balancing growth potential against capital loss risks. While stories of early Tesla/Nvidia investments inspire, success requires strategy and patience—never guaranteed outcomes.

In this guide, we explore risk-managed approaches like Pound Cost Averaging (investing fixed amounts regularly). This may help smooth market volatility but doesn't eliminate risk.

All investments risk capital loss. Past performance ≠ future results. Not personalised advice.

How to start a Stocks and Shares ISA?

Maximise Your Tax-Free Allowance

UK adults receive a £20,000 annual ISA allowance, while children are entitled to £9,000 through a Junior ISA. Despite wide availability, ISA uptake remains relatively low — with around 16% of adults and fewer than 10% of children currently using them.

Capital at risk. ISA eligibility and tax rules apply.

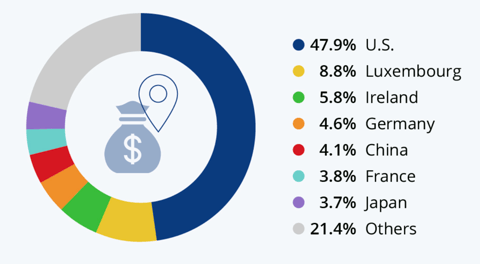

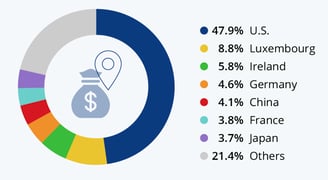

Understanding Index Funds

A globally diversified index fund within a Stocks & Shares ISA provides broad market exposure — helping reduce overreliance on single stocks and spread investment risk.

Think of an index fund like a jar of M&Ms — each sweet represents a company such as Apple or Microsoft. You effectively own a little of everything, in one wrapper.

Investor Considerations

Using the full ISA allowance (£20,000 for adults, £9,000 for children) equates to monthly contributions of roughly £1,666 and £750, respectively. However, many providers allow starting with £25 per month or less.

Past performance is not a reliable guide to future results. Investing involves risk, and values may fall as well as rise. Taking a long-term approach may help manage market volatility.

Choosing a Provider

Before investing, explore FCA-authorised platforms such as Fidelity, Vanguard, and Hargreaves Lansdown. These are examples only, not endorsements. Other providers are available.

Illustrative Scenario

Sarah, 35, uses educational resources to explore how index funds work, then decides to invest £500 per month in a global portfolio. This is a fictional scenario used for educational purposes only.

Capital at risk. This content is for general information only and does not constitute personal financial advice. Please consult a regulated financial adviser before making investment decisions.

Illustrative examples only. This does not constitute financial advice. We accept no responsibility for any decisions made based on this content.

Understanding the Benefits of Pensions for Long-Term Saving

When you're young, retirement may seem a long way off—but taking steps early can offer long-term financial advantages. Private pensions allow you to begin withdrawing from age 55 (rising to 57 in 2028), giving you flexibility in how you plan your retirement.

Most employees in the UK are automatically enrolled in a workplace pension, which includes contributions from both the employee and employer. In many cases, these come with valuable tax advantages. For example, the Annual Allowance for pension contributions in the 2025–26 tax year is £60,000 (subject to your income and other factors). Contributions receive tax relief, but higher- or additional-rate taxpayers may need to claim this through Self Assessment.

It’s also worth being aware of where your pension contributions are invested. Workplace pensions often use default investment funds, such as index trackers. While these funds aim to provide broad market exposure, they may not align with your personal values or risk appetite.

You can typically review or change your pension fund choices via your provider's online portal. Options may include UK equity funds, global index funds, or sustainable investment options, depending on what’s available in your scheme.

This article is for general information purposes only and does not constitute financial advice. Investment decisions should be based on your personal circumstances and, where appropriate, discussed with a regulated financial adviser.

Premium Bonds: A Chance to Win Tax-Free Prizes While Keeping Your Savings Safe

Premium Bonds from NS&I offer a unique way to save money—combining the security of government-backed savings with the excitement of a monthly prize draw. Instead of earning interest, your eligible bonds are entered into a draw where you could win tax-free prizes ranging from £25 to £1 million.

Unlike the lottery, your original money is secure. NS&I is backed by HM Treasury, which means your savings are protected. The minimum purchase is £25, and you can hold up to £50,000 in Premium Bonds. Bonds can also be bought as gifts for children.

However, Premium Bonds do not pay interest or guaranteed returns. If you don't win prizes, your money doesn't grow, and over time inflation may reduce its value in real terms.

This content is for general information only and does not constitute financial advice. Premium Bonds are not suitable for everyone, and returns are not guaranteed. Please consider your financial circumstances or consult a qualified adviser if unsure.

Illustrative examples only. This does not constitute financial advice. We accept no responsibility for any decisions made based on this content.

Precious Metals in Portfolio Diversification: Key Considerations

Gold, silver, and platinum are considered by some investors as non-traditional assets for portfolio diversification. Physical holdings require secure storage arrangements, while digital alternatives may be accessed via institutions such as the Royal Mint (mentioned here solely for illustrative purposes).

Market Characteristics and Industrial Demand

Historically, gold has shown distinctive market behaviour during periods of economic uncertainty. Silver plays a key role in renewable energy technologies, especially solar panels, while platinum is used in hydrogen fuel systems. These industrial applications can influence demand in ways that differ from traditional financial drivers.

Diversification and Risk Management Approaches

Diversification is a strategy some investors evaluate to spread risk, though it does not protect capital or guarantee returns. Dollar-cost averaging—investing fixed amounts regularly—is another approach sometimes used to mitigate timing risks. This article does not recommend specific allocation levels or endorse any investment strategy.

Key Risks and Tax Considerations

Precious metals are highly volatile and their prices are influenced by global economic trends, currency movements, and geopolitical events. Storage costs can reduce overall returns, and precious metals are not protected by the Financial Services Compensation Scheme (FSCS). According to FCA research, 67% of retail commodity investors incur losses. Capital Gains Tax may apply when selling assets at a profit.

Important Reminder

Before investing in precious metals, seek advice from an FCA-authorised financial adviser to determine suitability for your personal financial goals and risk profile. All investments carry a risk of loss, and past performance is not a reliable guide to future results.

Illustrative examples only. This does not constitute financial advice. We accept no responsibility for any decisions made based on this content.

Considering Individual Shares? Understand the Risks

Investing in individual shares involves significant risk and volatility. Share prices can fluctuate sharply, and this approach may not suit those who check their investments daily or are uncomfortable with short-term losses. Many retail investors buy when prices rise and sell during downturns, often locking in losses. Patience and a long-term perspective are key elements of disciplined investing. Share values can fall quickly, and capital is at risk.

Our Investment Approach

We follow a diversified strategy, typically holding around 35 shares to balance growth potential and dividend income. Diversification helps manage—but does not eliminate—risk. Investors may explore similar approaches or focus on individual companies with strong fundamentals. One possible tactic is phased investing: committing part of your funds initially and adding more if the share price drops 10–15%. This strategy does not guarantee profits or prevent losses.

Dividend Potential

Dividend-paying companies can play a role in long-term investment strategies. Reinvesting dividends may compound returns over time. However, dividends are never guaranteed and can be reduced or cancelled depending on business or market conditions. Past performance is not a reliable indicator of future results.

Long-Term Thinking

Consider sectors or companies you believe will thrive over the next decade. Avoid reacting to short-term market noise. Individual shares can offer growth but carry greater risk. Dividend strategies may provide income but are subject to change. Phased investment can lower entry prices but offers no protection against overall market declines.

Tax-Efficient Investing

You can invest up to £20,000 annually in a Stocks & Shares ISA without paying tax on gains or dividends, depending on your circumstances. Hargreaves Lansdown is one FCA-authorised provider offering access to shares, but this is not an endorsement—other platforms exist. Compare options carefully.

Educational Example

As a hypothetical scenario, you research a company and invest £500. If the share price falls 12%, you invest another £500, lowering your average cost. Over time, reinvested dividends may increase your position. This is an illustrative example only. It is not investment advice. All investing involves risk, including capital loss.

Important Disclaimer

This article is for general educational purposes only and does not constitute personal financial advice. ISA rules may change and depend on individual circumstances. Always consult a financial adviser regulated by the Financial Conduct Authority (FCA) before making investment decisions.

Mission Statement

Empowering your financial journey. We provide knowledge-driven strategies, actionable resources, and community support to help you work toward lifelong resilience.

Contact info

contact@asianrobinhood.com

Disclaimer: AsianRobinHood.com provides general, unregulated financial education and is not authorised or regulated by the Financial Conduct Authority (FCA) or any other UK financial regulator. The content on this site does not constitute personalised financial advice, tax guidance, or any other regulated service. Investing involves risk. Your capital is at risk and investments may lose their full value. Past performance is not a reliable indicator of future results.

You should always do your own research and, where appropriate, seek advice from a qualified professional who is authorised by the FCA. You can check whether a firm or adviser is regulated by visiting the Financial Services Register. We expressly disclaim all liability for any financial loss or decision made based on the content published on this site.

For more information, please review our Terms & Conditions, Full Disclaimer, Privacy Policy, and Transparency Statement.

© 2024. All rights reserved.