Banking & Savings

Navigating the world of banking can be overwhelming with the vast array of services available. From current accounts to credit cards and savings options, it can be challenging to identify which features best suit your individual needs.

Security is also a key consideration when managing your finances. UK-regulated banking institutions protect eligible deposits up to £85,000 per person, per authorised institution under the Financial Services Compensation Scheme (FSCS). While bank failures are rare, this protection is crucial for safeguarding your money.

In this section, we'll explore different types of banking accounts, highlighting key features and security aspects to consider. This information can help you understand the options available and compare products effectively based on your own research and circumstances.

Remember: This is general information, not personal financial advice.

Is American Express a Strong Option for a Credit Card with Excellent Customer Service and No Annual Fee?

American Express (AMEX) has become a respected name in the UK credit card market. While it was once accepted by fewer retailers, availability has grown significantly in recent years, especially online and in larger stores.

One of AMEX’s key strengths is its customer service. Many cardholders value the way it handles disputes. If a problem arises with a purchase and the retailer doesn't resolve it, you can raise a dispute through AMEX. In some cases, especially with smaller amounts, AMEX may resolve the issue quickly by crediting your account. While not guaranteed, this level of support is appreciated by many users.

Two AMEX cards that do not charge annual fees are the Cashback Everyday Credit Card and the British Airways American Express Credit Card. The Cashback card offers up to 1% cashback when annual spending exceeds £10,000. The BA card is popular with frequent travellers, offering a companion voucher after £15,000 in annual spend, which can be used for a second ticket on the same flight or for a 50% discount on selected Avios bookings. Both cards have premium versions that include more benefits, but these come with annual fees.

There are many credit cards available. Be sure to compare options and consider your personal needs before applying, either directly or through a regulated comparison website.

Not all retailers accept AMEX, so it’s worth checking before relying on it as your main card. As with any credit product, approval is subject to eligibility and your credit history.

Important: Always consider the representative APR, credit limit, and your ability to repay. Responsible use of credit can improve your credit score, while missed payments can harm it. This article does not constitute financial advice.

Illustrative examples only. This does not constitute financial advice. We accept no responsibility for any decisions made based on this content.

Is Chase a Leading Online Bank for UK Customers?

Since launching in the UK in 2021, Chase Bank has become a popular choice for those seeking a fully app-based banking experience. With no physical branches, all services are accessed via its mobile app, designed for ease of use and quick access to features.

Key highlights include:

Ease of Use & 24/7 Support: A user-friendly app paired with around-the-clock customer service.

Competitive Savings Rate: 2.75% AER on easy-access savings accounts (subject to change).

1% Cashback on Spending: Earn cashback on everyday card purchases (terms apply).

No Foreign Transaction Fees: Use your card abroad without additional charges.

5% Interest on Round-Ups: Earn 5% AER on round-ups to the nearest pound for 12 months (subject to limits).

Numberless Debit Card: A focus on security, with in-app card controls and the option to freeze your card instantly.

While Chase offers strong features, it may not suit those who prefer in-branch services or require complex banking products.

Important: Products are subject to status, eligibility, and terms. Rates and offers may change. This article is for general information only and does not constitute financial advice.

Chase is a trading name of JPMorgan Chase Bank, N.A., authorised by the Prudential Regulation Authority and regulated by the Financial Conduct Authority and the Prudential Regulation Authority.

Illustrative example only. This does not constitute financial advice. We accept no responsibility for any decisions made based on this content.

Savings Options from Investec: Easy Access, 90-Day Notice and 1-Year Fixed Accounts

Investec, a UK-based bank with over 50 years of experience, offers three types of savings accounts that may suit different savings goals: the Online Flexi Saver, 90-Day Notice Saver, and 1-Year Fixed Rate Saver. Each product offers a different balance between flexibility, access restrictions, and interest rate.

The Online Flexi Saver provides a variable interest rate of 4.20% AER, allowing you to access your money at any time without notice. This may appeal to those who want to earn interest while keeping their savings easily accessible.

The 90-Day Notice Saver currently offers a variable rate of 4.43% AER. Withdrawals require 90 days' notice, making this product more suitable for savers who can plan ahead and are comfortable with limited access to their funds.

The 1-Year Fixed Rate Saver offers a fixed interest rate of 4.40% AER. Funds are locked in for the full term, and early withdrawal is not permitted, so this may be appropriate for savers with longer-term goals who don’t need access to their money.

Interest earned may count towards your Personal Savings Allowance. If exceeded, tax may be due, and you may need to report it via Self Assessment.

Important Information: Eligibility and terms apply. Interest rates are subject to change or withdrawal. This article is for general information only and does not constitute financial advice. Investec Bank plc is authorised by the Prudential Regulation Authority and regulated by the Financial Conduct Authority and the Prudential Regulation Authority.

Illustrative examples only. This does not constitute financial advice. We accept no responsibility for any decisions made based on this content.

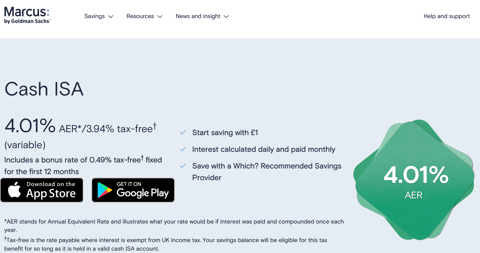

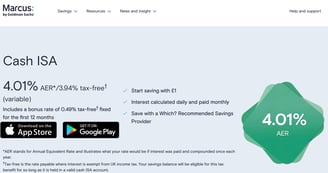

Marcus by Goldman Sachs: A Tax-Free Cash ISA Option

Marcus by Goldman Sachs offers a Cash ISA currently paying 4.01% AER (variable), providing a tax-free savings option for UK residents. While Goldman Sachs is globally recognised as an investment bank, it launched Marcus in the UK in 2018 to serve the consumer savings market.

A Cash ISA allows interest to be earned tax-free, which may be especially beneficial for higher-rate taxpayers. The current annual ISA allowance is £20,000 for the 2025/26 tax year, which can be allocated across different types of ISAs, including Cash ISAs and Stocks & Shares ISAs, subject to HMRC rules.

The Marcus Cash ISA may appeal to those seeking a straightforward, no-fee savings product. Withdrawals are permitted, but re-deposits will count toward your annual ISA allowance unless it’s a flexible ISA.

Your eligible deposits are protected up to £85,000 by the Financial Services Compensation Scheme (FSCS).

Important Information: Interest rates are variable and may change. Tax treatment depends on individual circumstances and may change. This article is for general information only and does not constitute financial advice. Marcus by Goldman Sachs is a trading name of Goldman Sachs International Bank, authorised by the Prudential Regulation Authority and regulated by the Financial Conduct Authority and the Prudential Regulation Authority.

Illustrative examples only. This does not constitute financial advice. We accept no responsibility for any decisions made based on this content.

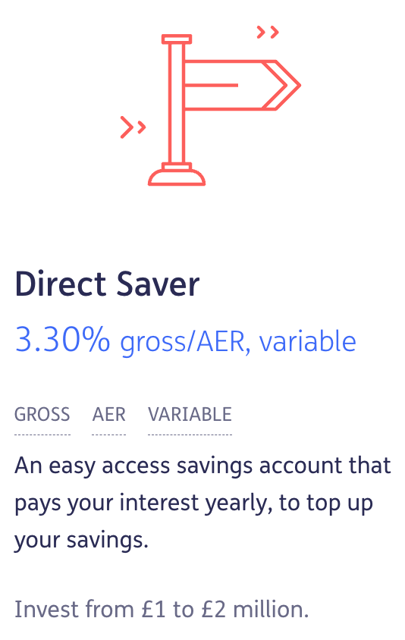

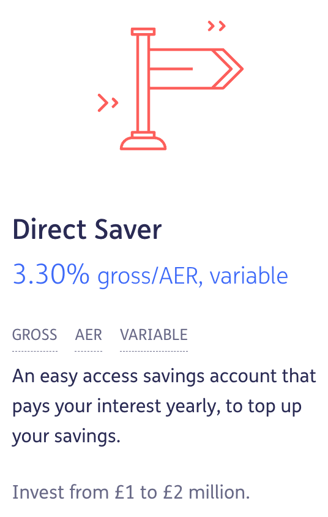

Looking for a High-Interest Easy Access Account with Government-Backed Security?

If you're fortunate enough to have substantial savings, you may be interested in the National Savings & Investments (NS&I) Direct Saver. NS&I is backed by HM Treasury, which means that all deposits are fully protected by the UK government—unlike standard bank accounts, which are typically protected up to £85,000 under the Financial Services Compensation Scheme (FSCS).

The NS&I Direct Saver allows deposits of up to £2 million, with an interest rate currently set at 3.3% (variable). While this rate is competitive, many savers are particularly drawn to the security of knowing that their full deposit is protected by the government.

NS&I also offers other easy access options, such as a Cash ISA, though the Direct Saver currently offers the most attractive rate for high deposit amounts. You may also wish to explore their Premium Bonds and other savings products, which we cover in more detail in our "Invest" section.

It's important to note that any interest earned above your Personal Savings Allowance may be subject to income tax. If this applies to you, you may need to declare the interest through a Self Assessment tax return with HMRC.

Illustrative example only. This does not constitute financial advice. We accept no responsibility for any decisions made based on this content.

Mission Statement

Empowering your financial journey. We provide knowledge-driven strategies, actionable resources, and community support to help you work toward lifelong resilience.

Contact info

contact@asianrobinhood.com

DISCLAIMER: AsianRobinHood.com delivers unregulated financial education only. We are not authorised or regulated by the Financial Conduct Authority (FCA) or any UK financial regulator. Capital is at risk - investments may lose value entirely and past performance never indicates future results. Content never constitutes personalised financial advice, tax recommendations, or regulated services. You must always consult FCA-registered advisors verified through the Financial Services Register before making any financial decisions. We expressly exclude all liability for financial losses arising from content reliance. Full terms governing liability exclusion are available in our Terms & Conditions and Full Disclaimer. Essential policies include our Terms & Conditions, Full Disclaimer, Privacy Policy, and Transparency Protocol.

© 2024. All rights reserved.